Precision Medicine’s Scaling Problem | Ep. 997

The More We Learn About Disease, The Smaller the Markets Become

Hello Avatar! Welcome to another week of biotech analysis. Today’s commentary, as always on Thursday, focuses on the general market update. For the week the XBI was up +1.77% and now sits at +9.62% year-to-date. This week confirmed the playbook. Biotech can rally and capital can return quickly, but funding is flowing to companies with clean catalysts and tight execution. Secondaries continue to dominate the financing landscape, while IPO activity remains scarce. Investors are rewarding near-term proof and punishing duration risk. In this environment, cost of capital shapes trial design, and clock discipline matters as much as mechanism.

We are now publishing 7x per week according to the following cadence:

Mondays: Stocks

Tuesdays: Biotech

Wednesdays: Podcast

Thursdays: Markets

Fridays: News

Saturdays: Podcast

Sundays: Strategy

We are also publishing unique content on X - be sure to follow up if you are not already @BowTiedBiotech. And to check-out the archive of our work on X you can find it on our website at: BowtiedBiotech.subtack.com/x-articles.

SUBSCRIBE TO PODCAST HERE:

Please help spread the work by subscribing and hitting the share button if you are enjoying content!

Lots to cover this week, let's get started!

BIOTECH PUBLIC MARKET UPDATE

For the week, the public indexes were MIXED, with the S&P +1.65% & DOW moving -0.27%. For the year the public indexed are UP the S&P is up +6.0% and DOW is up +2.2%. The XBI (the biotech index) comes in UP +1.77% for the week and is up +9.6% for the year.

Macro Update

The broader economy is moving from efficiency to resilience. That matters for biotech more than people think.

For 20 years the industry optimized around lean development. Outsource the CRO work. Centralize manufacturing. Depend on global CDMO networks. Keep fixed costs low. Move fast when capital is cheap and supply chains behave. That model worked when globalization felt stable.

That regime is changing.

Biotech now sits inside the same global reset affecting semiconductors, energy, defense, and AI compute. Supply chains are being judged less by lowest cost and more by reliability. The BIOSECURE Act has pushed companies to reassess China-linked outsourcing exposure, while U.S. radiopharma capacity remains constrained by isotope supply, hot-cell infrastructure, and specialized CDMO capacity. Cell and gene therapy faces the same problem in a different form. Manufacturing is growing, but the system still needs more flexible, localized, and automated capacity.

This changes how you should think about translation. Modern therapies are becoming too operationally fragile for the old hyper-efficient model. Precision medicine makes this worse. Smaller patient populations, tighter logistics, shorter treatment windows, specialized diagnostics, and complex manufacturing all reduce tolerance for disruption. A broad small molecule can absorb friction. A radiopharmaceutical, cell therapy, or biomarker-selected program often cannot.

The old model asked whether the drug worked. The new model asks whether the system around the drug can survive stress.

That is the macro shift. Biotech is moving from an efficiency economy to a resilience economy. The companies that matter will not only have strong biology. They will control manufacturing, diagnostics, logistics, and clinical workflows well enough to keep the therapy moving when the system gets tight. This is where the market still underprices risk. It still treats infrastructure as overhead. Increasingly, infrastructure is the product.

Introduction

This week we’re looking at a transition quietly reshaping the economics of biotech. Precision medicine improved the science. Clinical trials became cleaner. Response rates improved. Biomarkers helped companies identify the right patients with increasing accuracy. But every improvement in precision created a second-order effect the market still underestimates. Fragmentation. The better biotech becomes at defining disease, the smaller and more operationally complex each therapeutic market becomes. That changes everything from trial design and manufacturing to reimbursement and commercial scale. Most investors still analyze biotech using assumptions built during the blockbuster era. That framework is starting to break. The next generation of winners will not simply build better drugs. They will build systems capable of navigating increasingly fragmented patient populations and increasingly dynamic disease states.

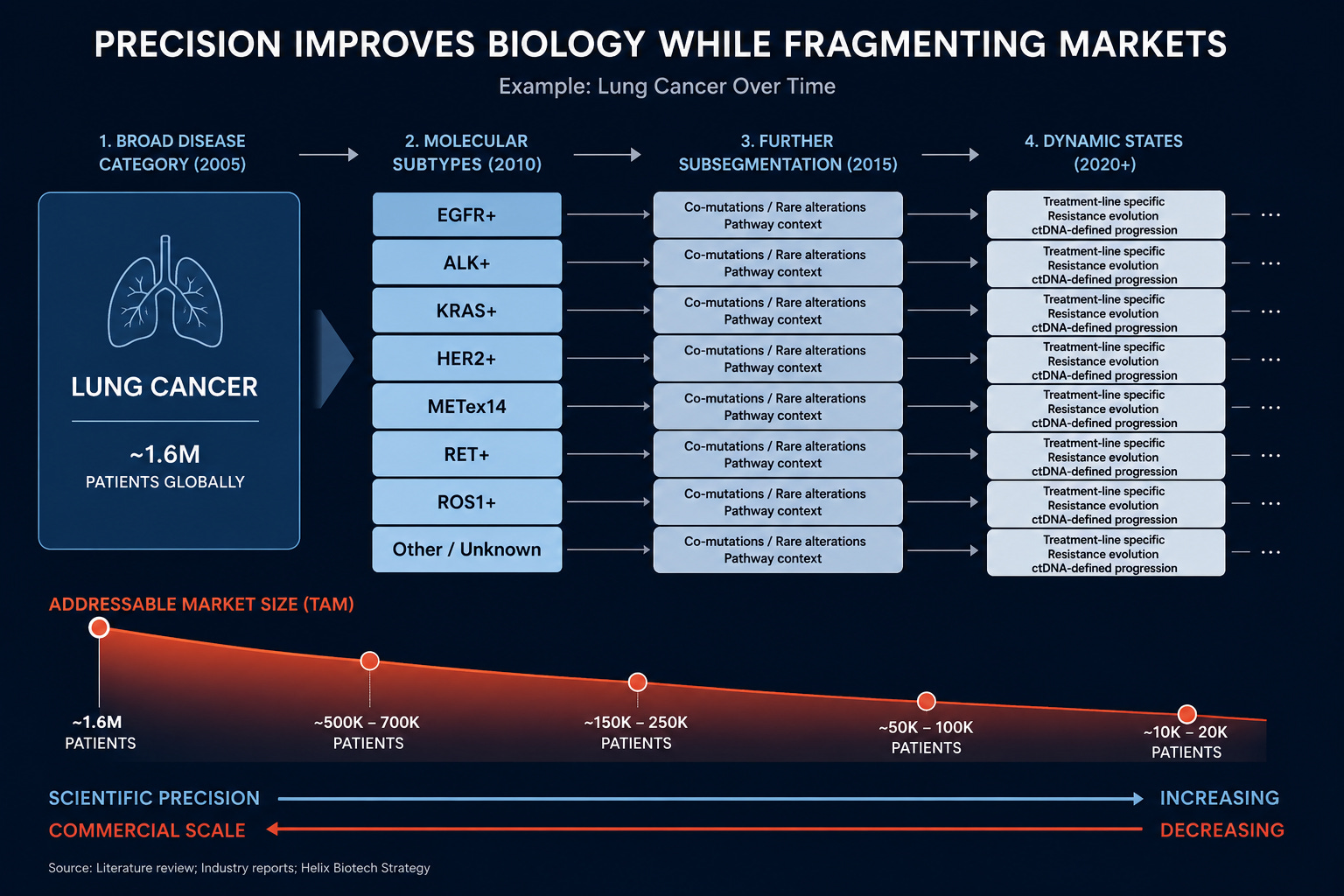

The Blockbuster Era Was Built on Broad Disease Labels

Biotech spent decades optimizing around broad disease categories. Large patient populations supported large commercial opportunities. Drug development, manufacturing, reimbursement, and sales infrastructure all evolved around this assumption. The blockbuster era rewarded therapies capable of reaching millions of patients through relatively simple prescribing frameworks.

Precision medicine changes that equation entirely.

Cancer already provides the clearest example. Lung cancer stopped behaving like a singular disease years ago. What once looked like a broad commercial category fractured into increasingly narrow molecular subsets defined by EGFR mutations, ALK rearrangements, KRAS mutations, HER2 amplification, MET exon skipping, and countless additional biomarkers layered on top of one another. Every improvement in classification improved the biology. Response rates improved because therapies targeted cleaner patient populations. Clinical development became more predictable. Regulators became more comfortable approving highly targeted drugs supported by smaller datasets.

At the same time, every layer of precision narrowed the addressable population.

That dynamic is no longer confined to oncology. It is spreading across autoimmune disease, neurology, metabolic disease, and rare disease. AI-driven stratification and increasingly sophisticated diagnostics continue pushing diseases into smaller biological categories. The market still tends to reward this trend as a pure positive because the scientific outcomes improve. But the economic consequences receive far less attention.

The more precisely biotech defines disease, the less scalable each market becomes.

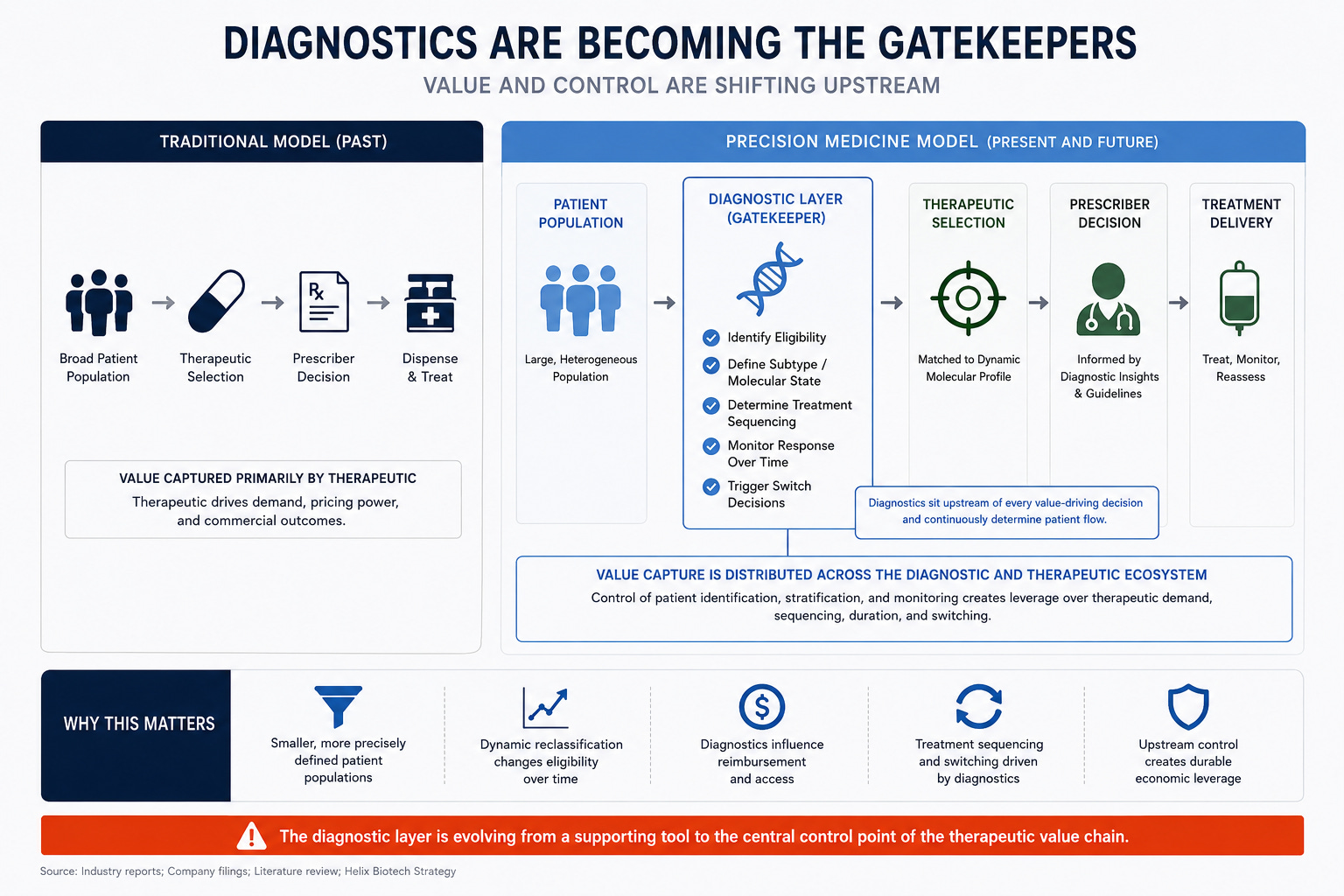

Precision Medicine Quietly Changed What a Drug Actually Is

The traditional pharmaceutical model treated therapeutics as standalone products. Precision medicine no longer functions this way. The therapeutic increasingly depends on an expanding infrastructure layer surrounding patient identification and disease monitoring.

Companion diagnostics, sequencing platforms, longitudinal biomarker analysis, molecular interpretation software, specialized treatment centers, reimbursement coding frameworks, and patient routing systems all become essential pieces of the therapeutic itself. The drug no longer operates independently from the system surrounding it.

That changes where leverage sits across biotech.

The market still tends to assign most of the value to the therapeutic company. Increasingly, however, the diagnostic layer controls patient access and treatment selection. This is already visible in oncology where biomarker testing determines eligibility, sequencing, and switching behavior. Therapies become dependent on upstream diagnostic infrastructure to generate demand.

The future winner is not always the company with the best drug. Sometimes it is the company controlling the classification system itself.

Diagnostics Are Becoming the Gatekeepers

The first generation of precision medicine identified patients once. A biopsy was performed, a mutation was found, and treatment was selected. That framework already looks outdated.

Liquid biopsy and fragmentomics technologies now allow continuous monitoring of disease states over time. Tumors evolve under therapeutic pressure. Resistance mutations emerge dynamically. Clonal populations shift throughout treatment. Disease classification itself becomes fluid rather than static.

This sounds incremental at first. It is not.

Biotech development still assumes relatively stable patient populations. Clinical trials are built around fixed inclusion criteria and static disease definitions. Commercial forecasts rely on reasonably stable market sizing assumptions. Regulatory frameworks operate around well-defined patient populations.

Liquid biopsy quietly destabilizes all of those assumptions.

The diagnostic layer now evolves faster than the therapeutic layer. A patient eligible for treatment today may fall into an entirely different molecular category six months later. Market size becomes dynamic rather than fixed. Enrollment becomes more difficult to predict. Reimbursement frameworks become harder to standardize because disease states continuously evolve underneath them.

Most investors are still underwriting biotech as though diseases remain relatively stable commercial categories. That framework increasingly breaks under modern precision medicine.

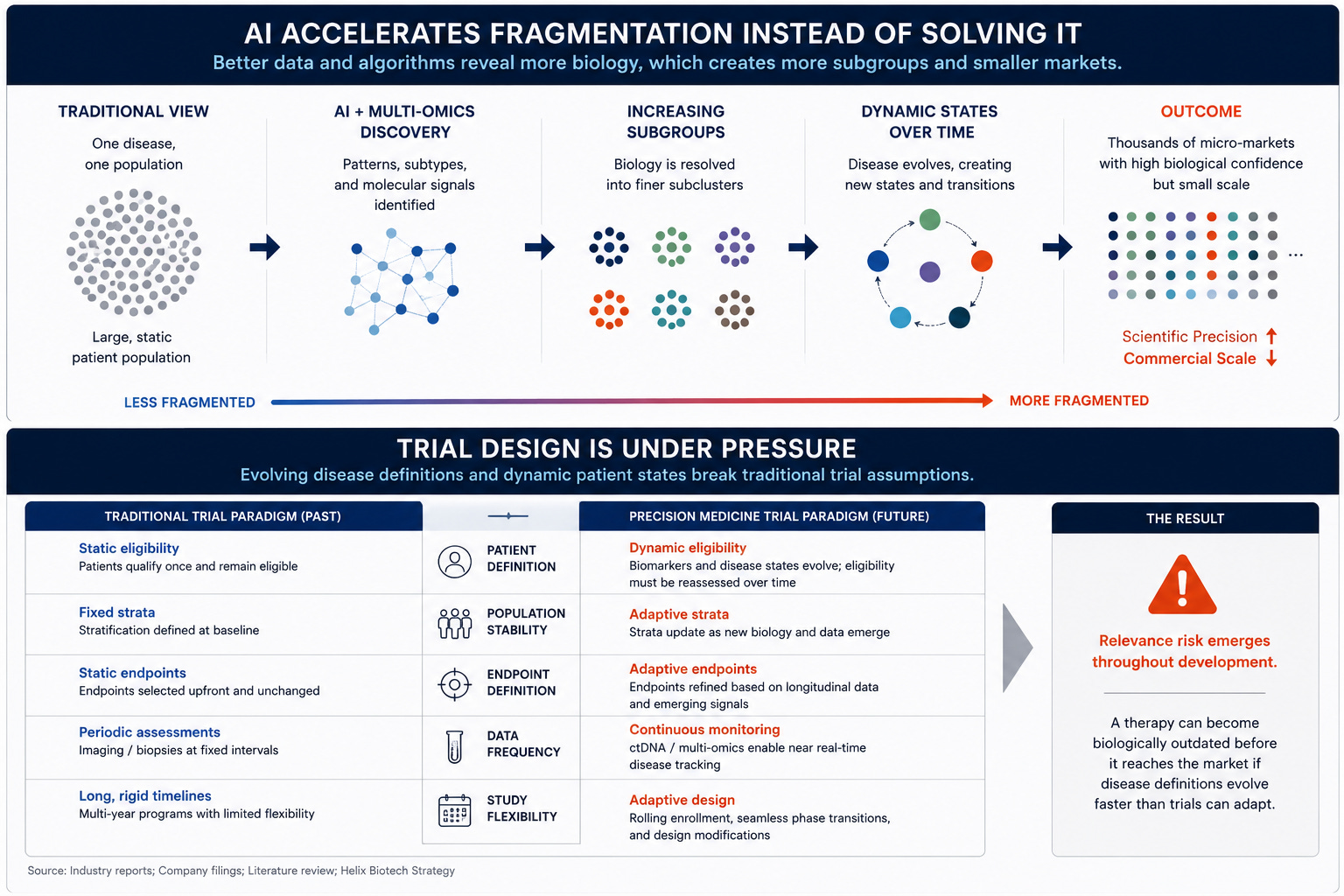

AI Accelerates Fragmentation Instead of Solving It

The market often frames AI as a tool that simplifies drug development and improves efficiency. In reality, AI may fragment disease categories faster than the industry can operationalize them.

AI systems excel at identifying hidden biological patterns across massive datasets. As these systems improve, they continue separating broad diseases into increasingly narrow molecular and phenotypic subgroups. That improves biological precision dramatically. It also shrinks commercial populations continuously.

This creates one of the most important contradictions in modern biotech. Scientific certainty improves while scalability weakens. The old biotech model rewarded therapies capable of addressing massive patient populations through broad prescribing patterns. AI-driven precision medicine increasingly creates thousands of smaller biologically coherent markets instead.

The endpoint of this trend looks very different from traditional pharma. Diseases stop behaving like static categories and start behaving more like continuously evolving molecular systems.

That transition creates enormous pressure on clinical development.

Trial Design Starts Breaking

Traditional trial design assumes reasonably stable disease definitions throughout development. Precision medicine destabilizes that assumption. Biomarker classifications evolve during studies. Molecular definitions shift faster than multi-year clinical timelines. Patient populations become harder to maintain consistently across development programs.

The result is growing friction between biology and regulation.

Future clinical trials likely look very different from the fixed designs dominating biotech today. Adaptive enrollment, rolling biomarker updates, longitudinal monitoring, AI-assisted patient stratification, and continuously evolving endpoint structures become increasingly necessary as disease definitions become more fluid.

This transition creates a new type of risk most investors still overlook. Approval risk no longer exists only at the end of development. Relevance risk emerges throughout the process itself. A therapy can become biologically outdated before commercialization even begins because the underlying classification system evolves too quickly underneath it.

That possibility becomes increasingly important as diagnostics improve.

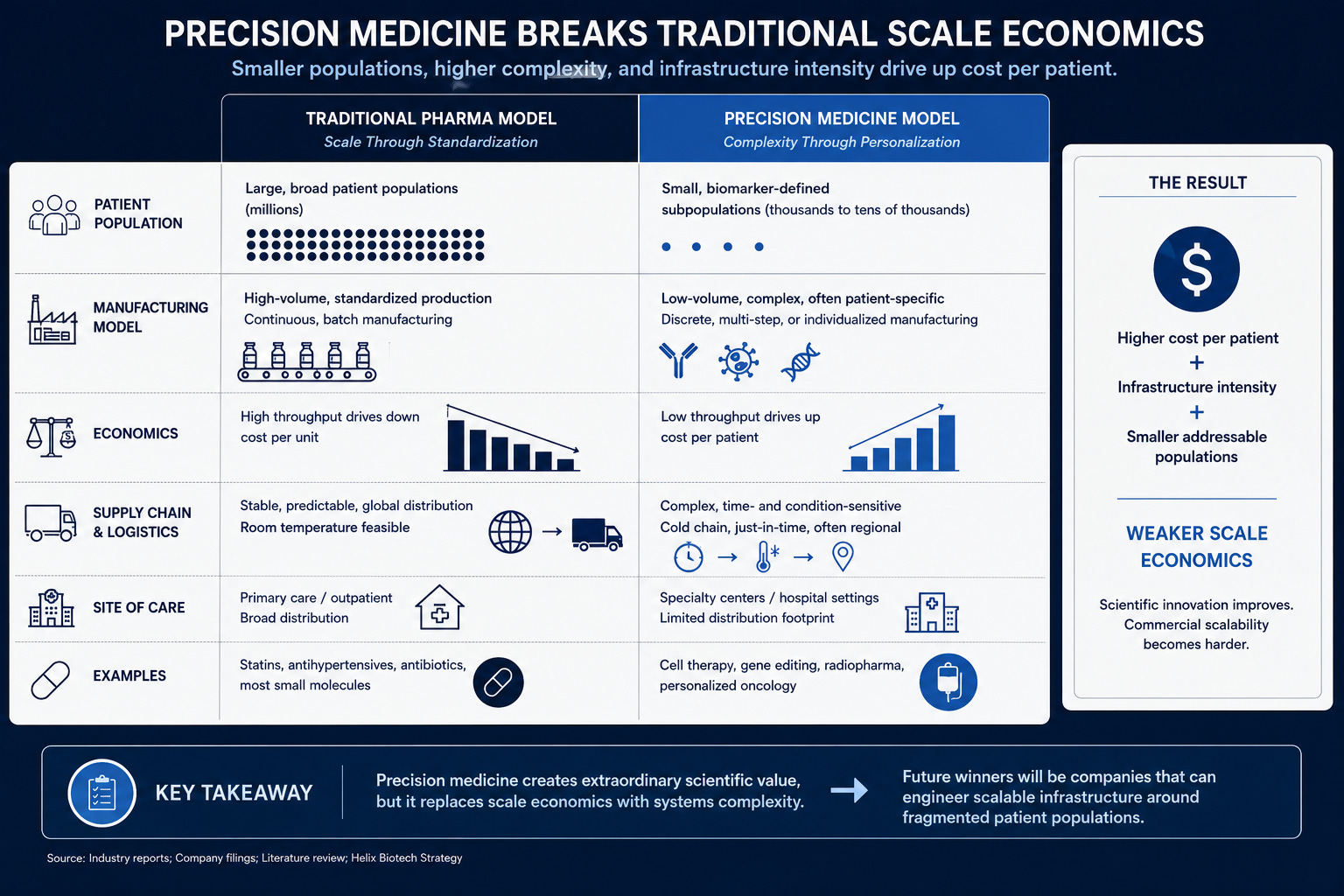

Manufacturing Economics Become Increasingly Difficult

Precision medicine breaks traditional pharmaceutical scale economics.

Large pharma manufacturing depends heavily on throughput and standardization. Precision therapies often move in the opposite direction. Smaller patient populations reduce manufacturing scale while increasing operational complexity.

This becomes especially obvious in cell therapy, radiopharma, gene editing, and highly stratified oncology programs. Many of these interventions function operationally more like specialized procedures than traditional pharmaceuticals. They require coordination across diagnostics, manufacturing, logistics, reimbursement, and administration infrastructure simultaneously.

The biology works. The operational model struggles to scale efficiently.

That distinction matters far more than most people realize.

Biotech spent decades assuming scientific success naturally translated into scalable economics. Precision medicine weakens that relationship. Therapies can produce extraordinary efficacy and still remain commercially constrained because the surrounding infrastructure becomes too fragmented and operationally intensive.

Biotech Is Quietly Splitting Into Two Industries

The industry now appears to be splitting into two distinct economic models.

One side still resembles traditional pharma. Obesity, diabetes, cardiovascular disease, and broad inflammatory markets continue depending on scale economics and large prescribing infrastructure. These markets still support blockbuster frameworks because patient populations remain broad enough to sustain them.

The other side increasingly revolves around fragmented precision interventions. Biomarker-driven oncology, radiopharma, gene editing, cell therapy, and rare disease all operate under very different constraints. These businesses increasingly resemble specialized systems engineering layered on top of biology rather than traditional mass-market pharmaceuticals.

Different infrastructure. Different economics. Different operational risks.

Yet public markets often continue valuing both models using remarkably similar assumptions.

That disconnect creates persistent mispricing across biotech.

Where the Market Misunderstands the Opportunity

Most investors still reward scientific precision without fully accounting for the fragmentation that follows. Higher precision improves efficacy, trial clarity, and approval probability. But it also creates smaller patient populations, reimbursement complexity, infrastructure burden, and growing dependence on diagnostics.

The next generation of biotech winners may not be the companies with the most sophisticated biology alone. Increasingly, the winners are likely the companies capable of reducing friction around precision medicine itself. Patient identification, workflow integration, adaptive diagnostics, longitudinal monitoring, and scalable infrastructure become increasingly important sources of leverage across the industry.

The therapeutic remains important. But it increasingly functions as one layer inside a much larger operating system.

That is the transition now underway across biotech.

Final Thought

Precision medicine solved one of biology’s hardest problems. It proved disease heterogeneity matters deeply and that better targeting improves outcomes. But every improvement came with a tradeoff. The more precisely biotech defines disease, the more fragmented therapeutic markets become. Diagnostics gain leverage. Trial design destabilizes. Infrastructure complexity expands. Commercial scalability weakens.

The science advances. The business model becomes harder.

Most investors still analyze biotech using assumptions built during the blockbuster era. That framework increasingly breaks under modern precision medicine. The next phase of therapeutic development will not be defined solely by better drugs. It will be defined by companies capable of integrating diagnostics, infrastructure, manufacturing, and adaptive patient classification into scalable systems.

If you focus only on efficacy curves, you miss the transition already underway.

If you follow the fragmentation, you start seeing where biotech is actually heading.

CONCLUSION

Today the takeaway is simple, even if the implications are not. Precision medicine solved a major scientific problem while quietly creating an economic one. The more precisely biotech defines disease, the more fragmented therapeutic markets become. Diagnostics gain leverage. Trial design becomes harder to stabilize. Manufacturing loses scale efficiencies. Commercial infrastructure grows more complex. The science improves while the business model becomes more difficult to scale. Most of the market still analyzes biotech using assumptions built during the blockbuster era. That framework increasingly breaks under modern precision medicine. The next generation of winners will not simply build better therapeutics. They will build systems capable of integrating diagnostics, infrastructure, adaptive patient classification, and scalable delivery around increasingly fragmented patient populations. If you follow the biology alone, you miss the transition already underway. If you follow the fragmentation, you start seeing where the industry is actually heading.

We are now publishing 7x per week according to the following cadence:

Mondays: Stocks

Tuesdays: Biotech

Wednesdays: Podcast

Thursdays: Markets

Fridays: News

Saturdays: Podcast

Sundays: Strategy

SUBSCRIBE TO PODCAST HERE:

Sundays and Mondays are under the paid umbrella, everything else is FREE. It is $11.99/month and we encourage you to support our efforts. It keeps us motivated to keep producing the hybrid science and business biotech focused content you will not find anywhere else all in the same place.

As a reminder, if looking to go deeper into the topics we cover check out our website BowTiedBiotech.com, or DM us on twitter, or email us: bowtiedbiotech@gmail.com

ABOUT BOWTIEDBIOTECH

As a reminder, the purpose of the BowTiedBiotech substack is two-fold. Primarily, we aim to provide our scientist audience the tools to build a biotech company and ultimately translate their ideas into medicines for patients. Secondarily, biotech investors may find this substack useful as we will be providing weekly market updates of the public AND private markets as well as heavily leveraging current financing events as teaching examples.

DISCLAIMER

None of this is to be deemed legal or financial advice of any kind. All updates are sourced from publicly available disclosures. Insights are *opinions* written by an anonymous cartoon/scientist/investor.